What is Buy Now Pay Later?

Buy Now Pay Later, or BNPL, is an emerging payment trend that allows customers to buy products or services in the present and pay for them in the future in installments. They are usually interest-free or carry very low interest. BNPL players offer customers easy instalment options without interest to encourage more purchases.

BNPL differs from EMIs in the sense that they have lower regulatory requirements and no interest. While zero-EMI options do exist, BNPL companies tend to offer more flexibility in terms of payments.

BNPL players tie up with retailers to provide the option to customers at checkout. If a customer chooses to use BNPL, they can also decide how they want to pay for their purchase over time. Repayment schedules and a number of instalments differ from one provider to another but usually come with more than one option.

For instance, you want to purchase a new laptop for $2000 by availing the services of a BNPL company. The laptop store may offer you the option to pay for the laptop over 12 months with instalments of $166 per month or over 24 months by paying $85 per month, a marginal interest included. This allows customers like you to make big-ticket purchases that you may not be able to afford upfront. At the same time, it helps retailers increase their sales.

BNPL Asia

Despite being a relatively new category in the region, BNPL in Asia, especially Southeast Asia, is booming. Based on a study by Mashable SE Asia, the BNPL market cap in the SEA region is set to grow from US$7.3 billion in 2019 to a whopping US$33.6 billion in 2027.

BNPL companies have gained a lot of following in Asia for numerous reasons. For instance, Asian consumers are extremely comfortable using credit products. Young shoppers entering the market tend to use credit alternatives to match high flung lifestyles. The rise of online shopping has also made buying things on credit easier.

Another reason why BNPL has taken off in Asia is that the regulations surrounding these products are still lax. This has led to BNPL players offering creative solutions to customers to encourage purchases. For instance, BNPL companies allow customers to buy products without having to pay interest for 12 months. Some others have the option to make partial payments and take the rest in instalments or defer payment for a while.

This increased flexibility has drawn young shoppers in, who look to BNPL as a way to make big purchases without getting into too much debt.

The Future of BNPL in Asia

Asia is dynamic, always at the forefront when it comes to fintech revolutions. The payments space is ripe with opportunities, and the eager young demographic in this region has made BNPL immensely popular.

Younger shoppers who do not have access to traditional credit are drawn towards BNPL solutions the most in Asia. Smaller fintech companies that dominate the lion’s share of the BNPL market in Asia are capitalizing well on this demand. For instance, Hoolah, a BNPL player in Singapore, uses data analytics to understand customer needs. Experts believe that BNPL will be the natural next step for payments in Asia. Here are some arguments that support that stance:

- Asia is home to one of the biggest and fastest-growing consumer markets globally. By the end of the decade, the continent will account for almost half of the world’s consumption growth – a $10 trillion opportunity. Companies want to empower people to buy better to capitalize on the spending power.

- BNPL is allowing shoppers to access high-volume retail segments that usually don’t offer credit e.g. cosmetics. Such segments are huge in Asia. Companies like Sephora are allowing customers to make cosmetic purchases in instalments.

- Southeast Asia still has an underserved financial services market despite having high mobile and internet penetration. Did you know that the region has 670 million consumers, but only 27% have bank accounts? BNPL plugs these gaps by offering low-friction, instant credit.

As the space garners more attention and attracts a higher consumer base, governments will start looking into regulation to prevent misuse and debt traps. For instance, Singapore issued a series of guidelines for consumers availing BNPL services to protect them against mounting debt.

Who Are The Top BNPL Players?

With the growing number of BNPL companies in Southeast Asia, the emerging sector is expected to dominate the region, with its eyes set on the massive underbanked and unbanked populations, in the years to come.

Here are some of the biggest BNPL companies to keep a look out for:

- Singapore: Atome, Shopback, Pace

- Indonesia: Akulaku, Kredivo, Indonana

- Vietnam: Reepay, Fundiin

- Philippines: Plentina, Cashalo, Tendopay

- Malaysia: Split, Pine Labs

BNPL companies in Singapore

Atome

The most mass market player out of the bunch, Atome has entered nine markets (namely Singapore, Vietnam, Indonesia, Thailand, Hong Kong, China, Malaysia, Taiwan and the Philippines) and boasts over 3,000 merchant partners across a wide range of categories since its launch in 2019. Some key partners include SHEIN, ZALORA, ZARA, Coach, Agoda, Nike, Adidas and MAC. It is the top BNPL player in Singapore. With Atome, you can expect:

- Zero interest

- Payments split into three instalments

- No hidden charges

- Online and offline shopping options

- An easy way to check the status of your payments on the app

Website: atome.sg

Hoolah (now ShopBack PayLater)

Hoolah, one of the most recognisable Singaporean-based BNPL startups, was acquired by ShopBack in 2022. Its BNPL services will now be called ShopBack PayLater. Shopback is present across Singapore, Thailand, Malaysia and Australia. In Singapore, it has over 2 million active users. Some of its key partners include Charles & Keith, VANS and Zalora.

- Available at over 4,000 offline and online merchants

- Zero interest on purchase

- Repayment in three equal instalments

- Offset your cashback and vouchers against payments

Website: hoolah.co

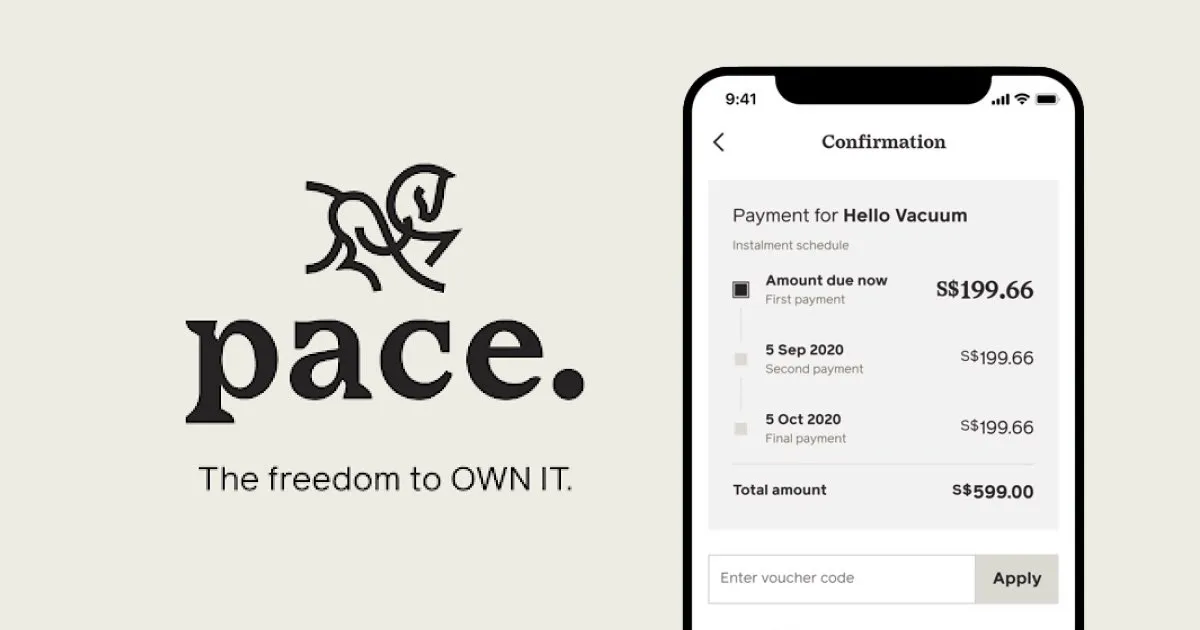

Pace Pay

Pace Pay began in Singapore in 2020, growing to be among the most trusted BNPL merchants in the region. It is available in Singapore, Malaysia, Hong Kong, Thailand, Taiwan, Japan and Korea. With Pace, you can expect:

- Zero interest

- Three instalment payments

- Three ways to pay - Pace App, Pace Card and Pace Chrome extension

- Earn reward points when you make purchases

Website: www.pacenow.co

BNPL companies in Indonesia

Akulaku

Akulaku is the top digital consumer finance platform and BNPL powerhouse in Indonesia. It has over 8 million active monthly users, 32 million registered users and a total of 295 million + platform transactions. Since its inception, the platform has serviced more than 90,000 merchants. Akulaku’s PayLater solution has been a game changer for many merchants and customers. Its top PayLater partners include Shopee, pegipegi, and Klik. It is also present in Malaysia and the Philippines. Here’s what you can expect:

- Interest-free instalments

- Paid in three instalments over three months

- Payments can be made using debit or credit cards

- Early repayment option available

Website: akulaku.com

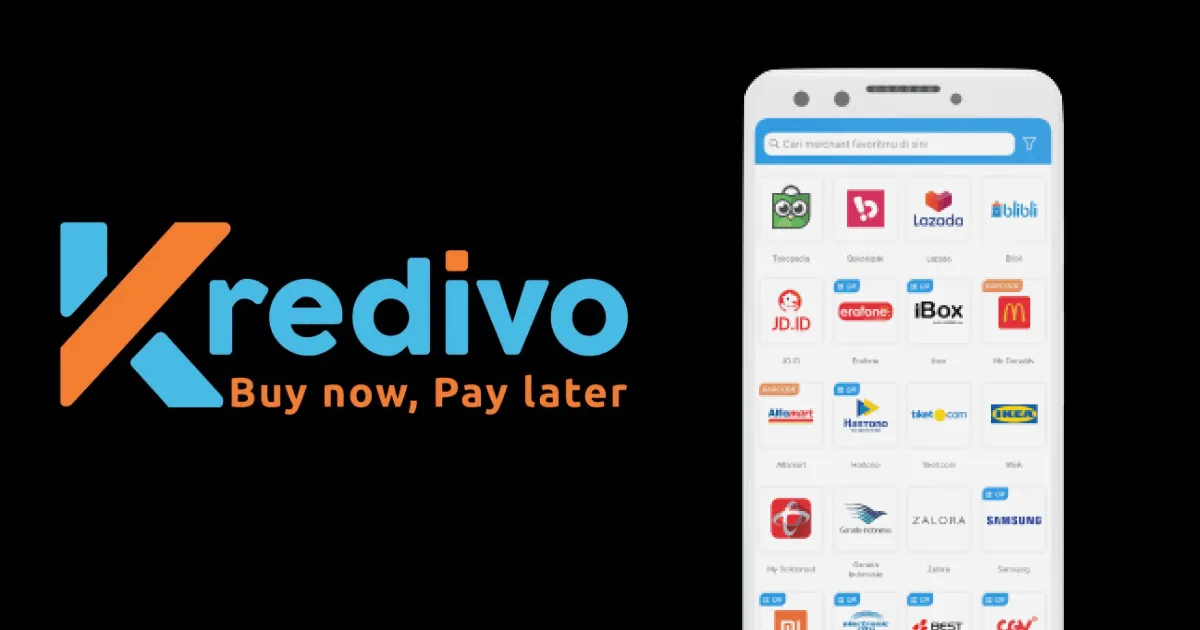

Kredivo

Launched in 2016, Kredivo, an Indonesia-based AI-enabled digital credit and lending platform, has made significant headway. Its BNPL solutions, while useful to alleviate the upfront cost of a purchase, are also seen as a way to build and improve one’s credit score. This is particularly impactful in Indonesia, where a majority of its population is under-banked with low credit card penetration. Currently, Kredivo has upwards of four million approved customers and secured merchant partnerships with eight out of the 10 top e-commerce platforms in Indonesia. It is also present in Vietnam. Here are its features:

- Payment option in three instalments

- Payment period for 30 days, 3 months, 6 months or 12 months

- Zero interest for up to 3-month instalments

- 2.6% interest per month for 6 or 12-month instalments

Website: kredivo.com

Indonana

Indonana has been operating in Indonesia since early 2018. The financial services platform’s PayLater feature has gained immense popularity since its launch. Through the platform, buyers can get access to up to 25 million rupiah credit in 62 cities and 35 provinces in Indonesia. Its leading partners include Tokopedia, Blibli and Tiket.com online, while it partners with over 1000 merchants offline.

Website: Indonana.id

BNPL companies in Vietnam

Reepay

Founded in November 2020, ReePay is one of the first BNPL players in Vietnam. Today, it is set to take the industry by storm. Since its inception, Reepay plans to target Vietnam’s 80 million consumers by boosting digital transactions, improving cash flow management, and ultimately helping drive business for ReePay’s merchants. Here are its features:

- Zero interest

- Repayment in four instalments

- Multiple payment options

- Quick onboarding

Website: ree-pay.com

Fundiin

Fundiin is a BNPL player in Vietnam that serves unbanked and underbanked customers in the country. In Vietnam, credit card penetration is only 5%. Fundiin plugs this gap by providing its instalment payment service at low fees and quick onboarding. The company has raised a total of $6.8 million, which it plans to use to penetrate more markets. Fundiin has partnered with more than 300 retail merchants having more than 4000 physical stores, including Mobile World, Unilever, Lug, Paula's Choice, etc. Here’s what it offers its customers:

- Three interest-free instalments

- No hidden fees or extra costs for on-time payments

- Profile approval in 30 seconds

BNPL companies in the Philippines

Cashalo

Cashalo is the first venture launched by Hong Kong-based fintech startup Oriente. Since the arrival of its mobile app in 2018, Cashalo has since evolved from targeting underserved Filipino customers with access to credit to cutting-edge BNPL solutions. Customers are able to complete their Cashacart profile and get pre-approval on their loan before shopping at one of the venture’s merchant partners. Together with the startup’s Finmas app in Indonesia, Oriente’s merchant partners experienced a 20% growth in sales volume. To date, the fintech boasts a combined total of 5 million users across the Philippines and Indonesia.

- Interest-free payments for up to 30 days

- Attractive offers and deals

- Online and offline payments

Website: cashalo.com

Plentina

Plentina is a young and rising fintech that is looking to ride the BNPL wave in the Philippines with a twist 一 the instalments can be paid directly and conveniently via e-wallets. Since its inception in October 2020, the app has had more than 30,000 downloads and raised US$2.2 million in its latest seed round. With plans to increase its merchant partners locally before setting its sight on expanding further across the SEA region, Plentina is focused on penetrating emerging markets where there’s a lack of credit score history. This is done via machine learning models to help determine a user’s creditworthiness. With Pletina, here’s what customers enjoy:

Website: plentina.com

Tendopay

TendoPay was founded in 2018 and is based in Makati, Philippines. It provides easy instalment payment options for e-commerce customers in the country. In December 2022, TendoPay was acquired by Tonik Bank. It partners with 500+ merchants online. Customers can:

- Pay in four easy instalments

- Shop online and offline

- Improve credit score

BNPL companies in Malaysia

Split

Backed by world-class investors, the likes of Silicon Valley’s 500 Startups, Entrepreneur First, as well as AccorHotels Asia Pacific Deputy CEO Louise Daley, Split gives its retailers access to customers from Malaysia’s local banks. The latest figures from the fintech saw RM10 million in total combined transactions for local retailers within a span of months. According to the folks at Split, its stable of more than 250 merchant partnerships is seeing a boost in revenue, sale conversions and traffic from offering its BNPL solutions to its customers. What can customers expect?

- Zero interest payments

- Up to three easy instalments

- No admin fees or late fees

- Shariah-compliant

Website: paywithsplit.co

Pine Labs

Pine Labs might just be the most senior company on the list, having been established as far back as 1998. Headquartered in Mumbai, India, has served over 40,000 merchants and over 6 million customers in Southeast Asia, India and the Middle East. To date, the fintech has racked up a combined US$3 billion in annualized BNPL transactions that are only looking to grow as it brings its Pay Later solutions to more countries across the region, such as Thailand and Indonesia. You can offer your customers:

- Zero interest instalment payment plans

- Payment through cards, digital wallets and even QR codes

- Cashback offers and discounts

Website: pinelabs.com

The BNPL Killers

Digital wallets and payment players across the world are noting the increasing lure towards BNPL. As a response, they are building their own BNPL options. Big names like Stripe and Square in the US are making headway into the instalment payment space. In Asia, Grab and PayPal are embedding their own split payment options within their app. So, how are these big players competing with smaller fintechs?

PayPal

For instance, Paypal’s CFO John Rainey commented in 2020 about its market share diminishing in areas where BNPL services are offered. As a result, the payments provider rolled out its own BNPL solution called Pay in 4, where consumers could settle payments in six weeks. In 2022, it launched ‘Pay Monthly’, another variation of the product that allows customers to pay monthly in six, 12 or 24 instalments. Paypal also acquired Japanese BNPL player Paidy to bolster its position in the Asian market.

Grab

Grab rolled out its pilot phase of BNPL products to Singapore customers. Following the pandemic, Grab realized the potential that online services had. With the pattern of more and more customers gravitating towards pay-later services, Grab introduced the feature on its app to tap into this market.

Stripe

American payments company Stripe also joined the BNPL war, partnering with multiple outlets to roll out its new feature for customers.

Established payment companies like Paypal, Grab and Stripe have an advantage, given their customer reach, merchant network and deep pockets. They will be in a better position to offer zero-interest instalments and other attractive offers to their customers. Smaller BNPL players will find it harder to match big league offers. While the BNPL space will continue to grow, the composition of top players is likely to shift from small fintech firms to established payment players and wallets.

Should You Use BNPL for Purchases?

BNPL is a good option for those who want to purchase big-ticket products but do not have the immediate bandwidth to make the purchase. It is especially useful if you don’t have a credit card. The BNPL feature is easy to use and takes just minutes to sign up. It is also cheaper than credit cards because of the extremely low interest.

Another advantage of BNPL is that it doesn’t affect your credit score. Even if you miss a payment, it does not reflect on your credit score because it is considered a short-term financing product. Similarly, you can’t use BNPL products to build your credit score.

On the flip side, if you do not keep track of the number of purchases you make with different BNPL players, you may find yourself raking up too much debt.

BNPL may be a good choice for you if you need to make a purchase immediately without paying high interest. However, you need to have the discipline and bandwidth to make payments on time because otherwise, you may end up paying a high late fee.

Final Word

BNPL companies are fast growing in Southeast Asia because of their convenience and low fees. If you want to make BNPL purchases, you should be careful of the terms and conditions that BNPL players provide.

If you are looking for a BNPL alternative to make your business purchases, check out the Aspire Advance Card. You can get up to 51 days of interest-free credit. Use the card to pay for inventory, ads, subscriptions or vendor payments.

.webp)

.webp)